| A Boutique Commercial Mortgage Brokerage, Dedicated to

Exceptional Service and Proven Results | |

Capital Markets Report | |

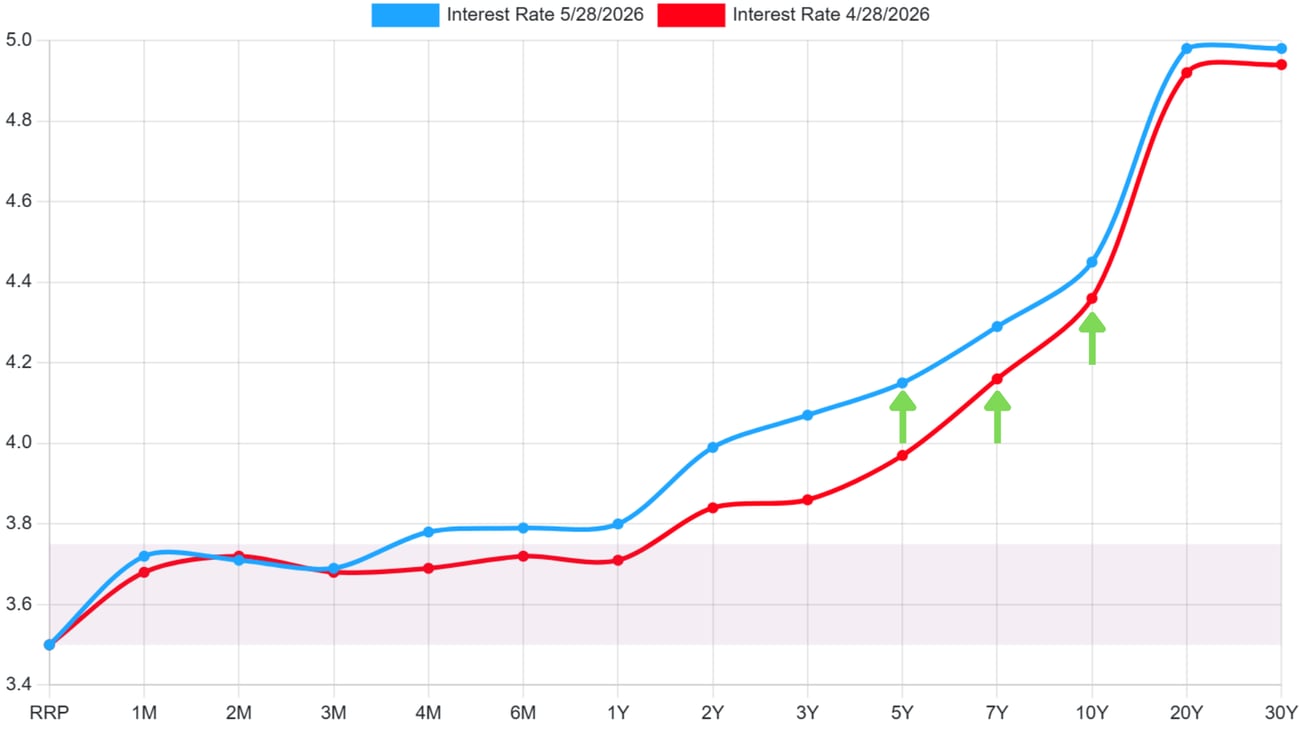

| | US Treasury Yield Curve

Month over Month Comparison |

|

|

|

|

|

|

In The News

|

|

Commercial Interest Rates and Bond Market Update

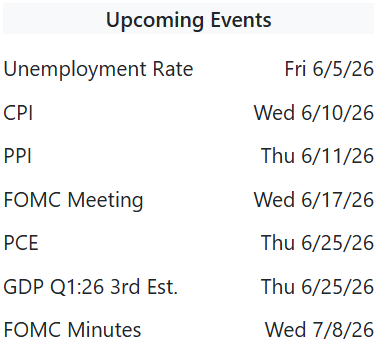

Week Ending May 29, 2026 Federal Reserve Policy

- The next FOMC meeting is June 16 to 17, 2026; no rate change is expected, with markets assigning near zero probability to a cut amid persistent inflation above the 2% target.

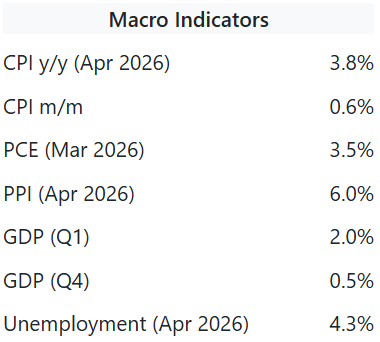

- April PCE data released this week showed softer than expected monthly readings, but annual headline and core PCE remain elevated at 3.8% and 3.3%, keeping the Fed on hold.

- The Fed's April 29 decision to hold rates at 3.50% to 3.75% passed on a divisive 8 to 4 vote, the most dissents since 1992, with some members openly raising the prospect of rate hikes.

Bond Market Trends

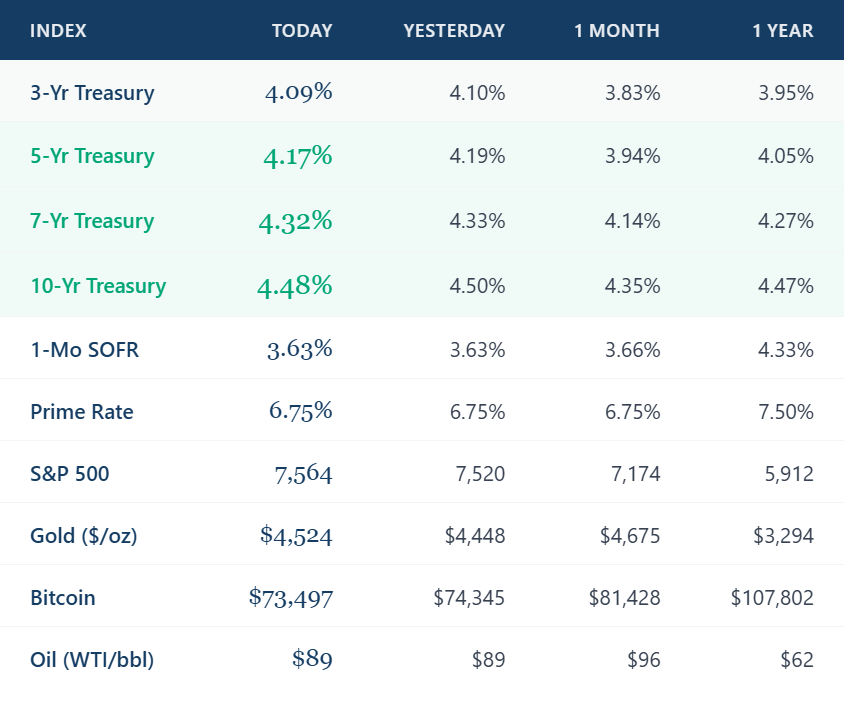

- The yield curve steepened month over month: the 5Y rose from 3.97% to 4.15% (up 18 bps), the 7Y from 4.16% to 4.29% (up 13 bps), and the 10Y from 4.36% to 4.45% (up 9 bps), reflecting growing term premium and fiscal concerns.

- Yields were pushed higher by record Treasury issuance, a widening federal deficit, Moody's recent US credit rating downgrade, and the Fed's hawkish split vote signaling potential rate hikes.

- A tentative US Iran ceasefire extension reduced energy price pressures late in the week, pulling the 10Y off its monthly highs and providing modest near term relief to long end yields.

Commercial Interest Rates

- Agency multifamily (Fannie/Freddie) loans are pricing 5.54% to 6.50% depending on LTV and term; HUD/FHA remains the lowest cost execution for stabilized assets with 80% or higher LTV.

- Construction and bridge financing is ranging 7% to 10%+, with lenders requiring tighter DSCR and lower LTC thresholds amid elevated short term rates and slowing development activity.

- CMBS conduit loans are pricing around 6.46%; life company lenders offer sub 6% execution for low leverage Class A deals, widening the spread advantage for well capitalized sponsors.

Takeaway: Treasury yields across the 5, 7, and 10 year maturities moved meaningfully higher this month, reinforcing elevated long term borrowing costs with no Fed relief in sight before year end. Sponsors with maturing debt should act now on refinance options, prioritizing agency and HUD execution to lock in certainty ahead of any further yield curve steepening.

LA Commercial Real Estate Market TrendsWeek Ending May 29, 2026 Multifamily

- Kilroy Realty sold two Hollywood apartment towers, Columbia Square Living (200 units) and Jardine (193 units), for $202M in gross proceeds closing in April at approximately $519K per unit.

- Onni Group filed plans to convert the Wilshire Courtyard office complex at 5700 Wilshire into twin 67 story residential towers delivering 2,586 units above 56,000 SF of retail space.

- Measure ULA carve outs under consideration at City Hall could reduce transfer tax revenue by up to 35% annually, potentially improving deal flow for transactions above $5.4M.

Retail

- Hollywood retail is rebounding with over 150K SF of new leasing commitments in the past six months, led by restaurants, nightlife, and wellness operators along Sunset and Hollywood Boulevards.

- Landlords are accelerating deal closings by offering aggressive TI packages and rent concessions, with free rent and below market base rents being used to attract the right credit tenants.

- Target anchored retail centers are still closing in the broader LA region despite softening consumer sentiment, with necessity based and experiential tenants leading absorption activity.

Industrial

- Neros leased 265K SF of sublease space in Torrance Pacific Gateway and Varda Space Industries leased 200K SF of the former Mattel Design Center, anchoring South Bay industrial demand.

- LA industrial vacancy edged up to 5.9% in Q1 2026 with asking rents averaging $1.39 per SF NNN, down 8.6% year over year as pricing adjusts, though South Bay remains among the tightest nationally.

- Tejon Ranch and Dedeaux Properties commenced a 510K SF industrial development in May, as defense, aerospace, and advanced manufacturing demand continues to drive South Bay expansion.

Office

- Kilroy Realty filed suit against bankrupt NeueHouse for $5M in unpaid rent at Columbia Square in Hollywood, highlighting ongoing tenant credit risk in flexible and hospitality branded office product.

- Onni's $408M CMBS loan on Wilshire Courtyard entered special servicing ahead of its July balloon maturity, with the borrower pivoting to a residential conversion as a potential workout strategy.

- LA's newly expanded Citywide Adaptive Reuse Ordinance is accelerating office to residential conversions; one DTLA high rise is already converting nearly 700 units under the streamlined approval process.

LA Market Takeaway: LA's CRE market continues to bifurcate sharply by asset class and quality, with industrial and well located retail attracting disciplined capital while office distress deepens. Multifamily fundamentals remain sound despite DTLA softness, with institutional scale residential pivots signaling long term conviction in LA's housing demand story. |

|

|

| A Lesson Beyond Brokerage

| |

The US is the World's #1 Oil Producer And What It Means for Your Deal

|

|

| Many investors are surprised to learn the United States is the single largest oil producer on the planet, surpassing Saudi Arabia and Russia. Since the shale revolution of the early 2010s, domestic output has transformed America from an energy importer into a global export powerhouse.

Why does this matter to commercial real estate? Energy prices directly drive inflation. When oil is expensive, transportation, construction materials, and operating costs all rise, pushing CPI higher and forcing the Fed to hold rates elevated longer. We saw this play out in real time this year, with Iran conflict fears spiking energy costs and keeping Treasury yields stubbornly high. Conversely, when US production ramps up and global supply increases, energy prices moderate. That softens inflation, gives the Fed room to cut, and brings long end Treasury yields down, which is exactly what loosens the commercial lending environment.

For borrowers and investors, understanding oil is understanding the rate environment. A ceasefire, a production increase, or a supply shock can move the 10 year Treasury by 20 to 30 basis points almost overnight, directly repricing every acquisition and refinance on your desk. Energy is not a separate conversation from real estate. It is the upstream variable driving the cost of your capital. |

|

|  |

|

|

|

|

|

|