| A Boutique Commercial Mortgage Brokerage, Dedicated to

Exceptional Service and Proven Results | |

Capital Markets Report | |

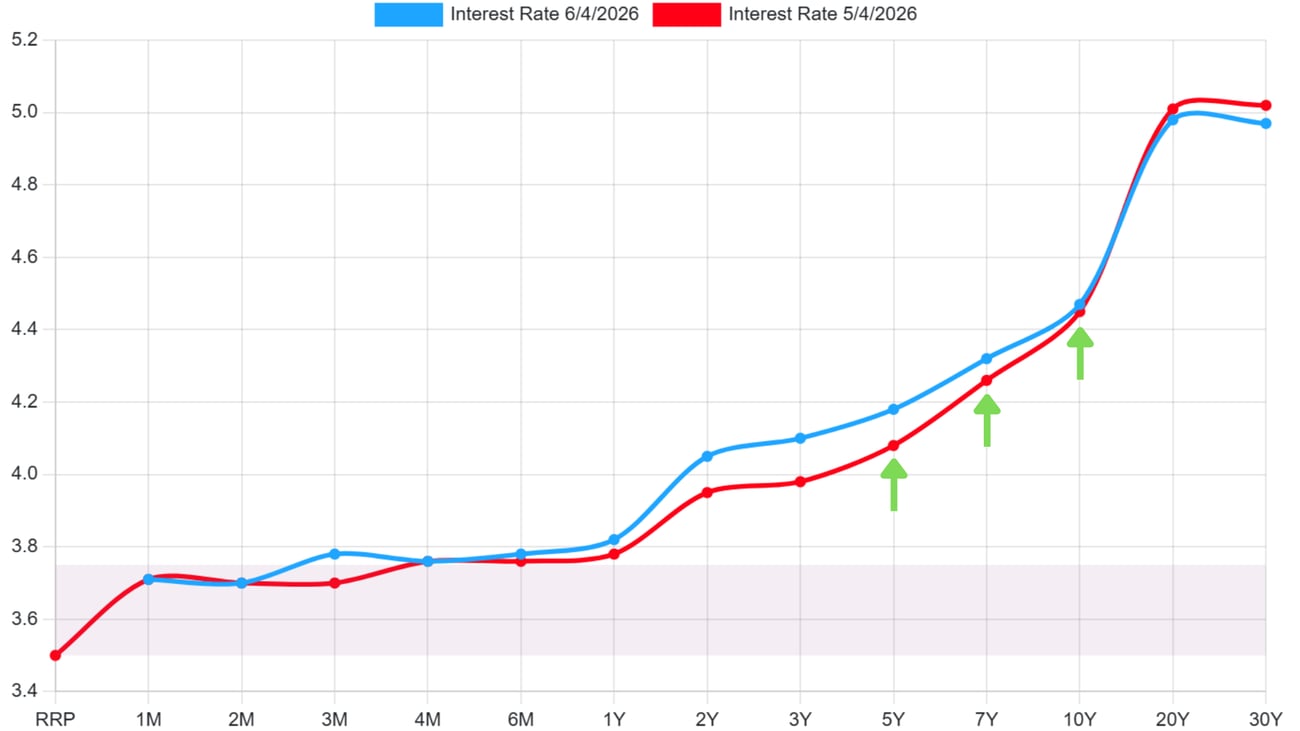

| | US Treasury Yield Curve

Month over Month Comparison |

|

|

|

|

|

|

In The News

|

|

Commercial Interest Rates and Bond Market Update

Week Ending June 5, 2026 Federal Reserve Policy

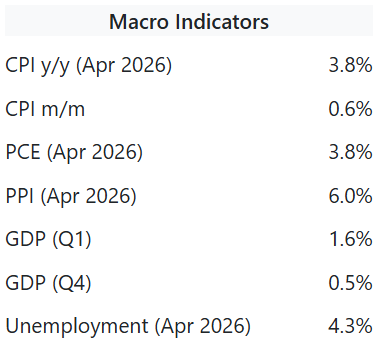

- The FOMC meets June 16 to 17 with no rate change expected. Markets have pushed the first cut to mid-2027, with BofA and several major brokerages forecasting zero cuts in 2026 amid sticky inflation above the 2% target.

- May CPI and PCE readings are due this month and will be closely watched. Energy costs tied to the Middle East conflict remain the primary inflation driver, keeping PCE persistently elevated above the Fed's 2% target.

- May payrolls released today (June 5) are expected to confirm continued labor market resilience. Strong jobs data would cement a hawkish Fed posture and raise market odds of a potential rate hike by Q4 2026.

Bond Market Trends

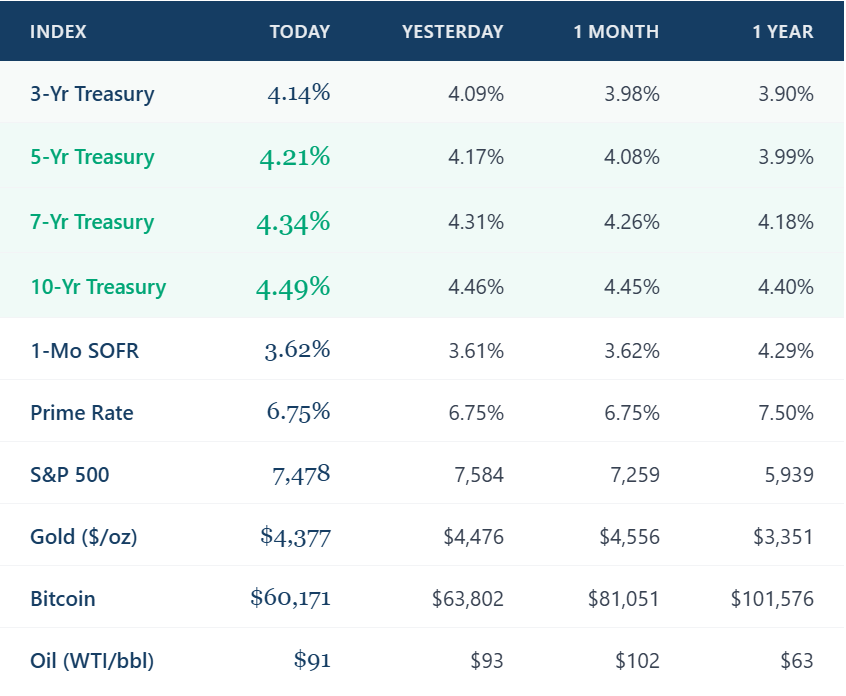

- The 5-Year Treasury rose to 4.18% (up 10 bps MoM), the 7-Year to 4.32% (up 6 bps), and the 10-Year to 4.47% (up 2 bps), reflecting a bear-flattening trend as inflation and geopolitical risk premiums build at the intermediate end.

- Persistent Middle East tensions and elevated oil prices drove yields higher mid-week. A partial Thursday rally tied to ceasefire hopes between Israel and Lebanon provided brief relief before yields stabilized at elevated levels.

- The yield curve remains positively sloped but compressing at the long end. With 20Y and 30Y yields near 5.00%, long-dated inflation concerns are widening Treasury spreads on floating-rate and short-term CRE debt structures.

Commercial Interest Rates

- Agency multifamily (Fannie/Freddie) rates open at 5.56% to 5.96% with up to 80% LTV on stabilized assets. Life company executions remain the most aggressive, sub-5.56% for low-leverage Class A primary market deals.

- Construction and bridge lending ranges 7.50% to 10.00%+ depending on leverage and sponsor. CMBS pricing holds near 6.47%, offering non-recourse fixed-rate execution for retail and industrial permanent debt.

- SBA 504 loans remain competitive at 5.88% up to 90% LTV for owner-occupied CRE. Mixed-use and retail strip centers price at 5.75% to 6.50% conventional; lenders are tightening DSCR floors to 1.30x on retail product.

Takeaway: Intermediate Treasury yields rose 6 to 10 bps month-over-month, compressing debt service coverage on newly underwritten deals. With the Fed on hold through at least mid-2027 and a rate hike scenario re-entering market conversation, borrowers should prioritize agency execution and fixed-rate lock-ins where available to protect long-term cash flow.

LA Commercial Real Estate Market TrendsWeek Ending June 5, 2026 Multifamily

- Avison Young is marketing a 190-unit Class A multifamily portfolio in Echo Park. Marcus and Millichap closed 61 units in Brentwood for a combined $46.35M, reflecting continued institutional demand for core LA submarkets.

- LA apartment loans are pricing at 5.54% to 5.96% (sub-$6M) with up to 80% LTV. Cap rates for stabilized assets hold at 4.75% to 5.25%; NOI growth of approximately 3.8% YOY supports current leverage for well-positioned assets.

- The RSO amendment capping annual rent increases at 4% takes effect July 1, 2026, compressing NOI growth capacity. Owners are accelerating exit timelines before the new formula activates, boosting short-term transaction velocity.

Retail

- Cedars-Sinai acquired the Beverly Connection shopping center for medical office conversion, signaling ongoing repurposing pressure on mid-market retail. Food, beverage, and service tenants continue absorbing quality inline space across LA.

- Stabilized grocery-anchored centers trade at 5.50% to 6.25% cap rates; lenders require DSCR floors of 1.30x and 65% to 70% LTV. Soft goods tenants face lease renegotiations as consumer credit stress and elevated delinquencies persist.

- Net effective rents are softening with landlords offering 12 to 18 months of TI concessions to secure longer WALTs. Sale-leaseback structures are gaining traction for credit-tenant retail assets seeking to free up balance sheet capital.

Industrial

- Breakthru Beverage signed a full-building 521,091 SF lease at PGIM's Shoemaker Business Park in Santa Fe Springs, one of the largest LA industrial deals of the cycle, reinforcing South Bay submarket strength and logistics demand.

- Industrial assets trade at 4.50% to 5.00% cap rates at approximately $385/SF. Permanent financing available at 5.75% to 6.25% at 65% to 70% LTV with 1.30x DSCR. LA industrial vacancy holds at 3.8%, among the tightest nationally.

- California AB 98 (2026) logistics regulations and tariff-driven supply chain shifts add near-term uncertainty. E-commerce and port-driven demand remain structural tailwinds, particularly in the South Bay and Commerce corridors.

Office

- Uncommon Developers acquired 601 S. Figueroa St. (Figueroa at Wilshire) for $210M ($201/SF), the largest LA commercial sale since early 2024. Colliers retained the leasing and management assignment for the 1.04M SF, 52-story DTLA tower.

- Office cap rates range 6.50% to 7.50% for stabilized assets; lenders require 50% to 55% LTV with significant reserves. Seller financing is re-emerging at the mid-market level as conventional debt remains constrained for non-trophy office.

- Onni Group is converting its Miracle Mile office project to residential, the latest adaptive reuse under the expanded ARO. Angel City Football Club renewed approximately 14,400 SF at Media Park Santa Monica, reflecting West LA's leasing resilience vs. DTLA.

LA Market Takeaway: LA's CRE market continues to bifurcate: industrial and multifamily retain strong fundamentals with institutional capital actively deploying, while office faces structural repositioning pressure and the RSO amendment adds urgency to multifamily exit timelines. Rising intermediate Treasury yields are compressing deal economics across all asset classes, making disciplined cap rate underwriting and fixed-rate execution essential in the current rate environment. |

|

|

| A Lesson Beyond Brokerage

| |

What Jane Street Teaches Us About Markets

|

|

| Most people have never heard of Jane Street. They do not manage your money, run ads, or ring the opening bell. Yet in Q1 2026, they generated a record $16.1 billion in trading revenue, more than double their haul from Q1 2025, cementing their status at the top of Wall Street's trading desks.

So what do they actually do? Jane Street is not a hedge fund. It does not take directional bets on markets going up or down. It is a market-making machine, a technology and quantitative research operation that profits when markets are liquid, deep, and active, and profits more when markets are volatile, because volatility widens the spreads that market makers earn on every trade. The trading function that was once the exclusive domain of investment banks has migrated to technology-first firms that can do it faster, more accurately, and at lower cost.

The lesson for CRE professionals: the firms quietly winning in any market are the ones with superior information, faster execution, and disciplined systems, not the loudest voices. Jane Street is now building its own data center to scale its AI compute capacity, doubling down on infrastructure while others celebrate last quarter's results. Speed, data, and process win. In any market. |

|

|  |

|

|

|

|

|

|