Commercial Interest Rates and Bond Market Update

Week Ending June 19, 2026 Federal Reserve Policy

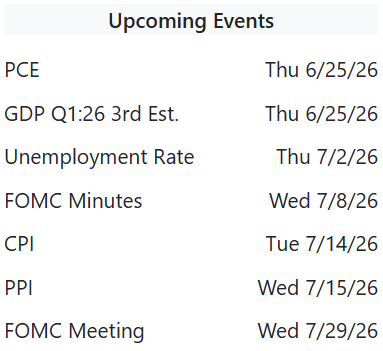

- The next FOMC meeting is July 28 to 29, 2026; markets also await the June CPI release on July 14 and May PCE data on June 25, both critical inputs for the Fed's next rate decision.

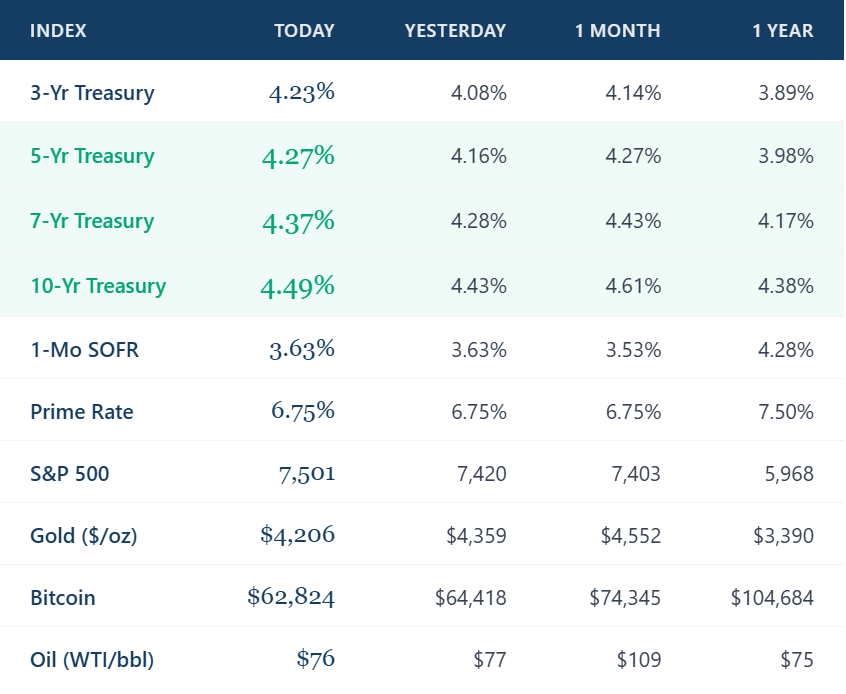

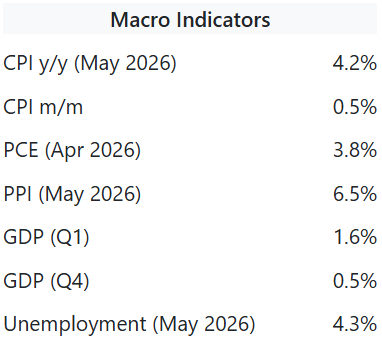

- May CPI came in at 4.17% year over year; April PCE headline was 3.77% with core PCE at 3.29%, both well above the Fed's 2% target and reinforcing the current hold posture.

- At the June 16 to 17 FOMC, Chair Warsh held rates at 3.50% to 3.75% and removed cut bias language; the dot plot now signals a possible hike to 3.8% by year end, shifting market pricing toward tightening.

Bond Market Trends

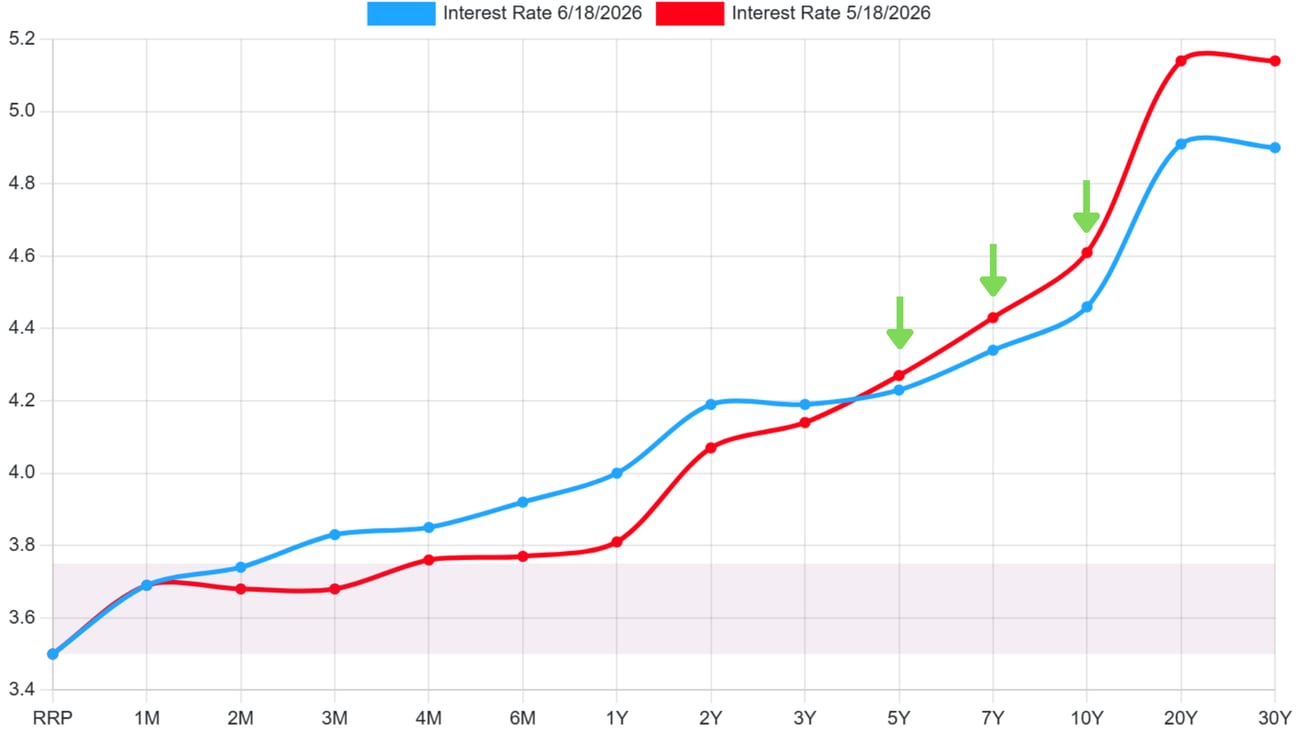

- Month over month Treasury yields declined: the 5Y fell from 4.27% to 4.23% (4 bps), the 7Y dropped from 4.43% to 4.34% (9 bps), and the 10Y eased from 4.61% to 4.46% (15 bps).

- Post FOMC hawkish commentary from Chair Warsh, removing cut guidance and signaling a possible hike, briefly pushed 10Y yields up 6 bps on June 17; energy driven inflation remains the key upside risk to rates.

- The 30Y Treasury fell from 5.15% to 4.90% month over month (25 bps), signaling easing long duration risk premium; this compression benefits life company and CMBS executions on stabilized CRE assets.

Commercial Interest Rates

- Agency executions (Fannie/Freddie) open at 5.52% to 5.60% for 5 to 10 year fixed, up to 80% LTV non recourse; FHA/HUD at 5.55% for stabilized multifamily over $3M with full term interest only available.

- Construction and bridge financing prices at 7.50% to 9.00% over SOFR; lenders requiring 1.25x DSCR minimums and tighter LTC ratios as rising cost of funds compresses project level returns.

- CMBS pricing at 6.32%; life company executions at 6.00% for long term fixed on retail and industrial; SBA 504 at 5.88% remains competitive for owner users; debt yield remains the primary underwriting constraint.

Takeaway: Despite month over month Treasury yield declines across the 5Y to 30Y curve, the Fed's hawkish pivot under Chair Warsh and persistently elevated PCE and CPI readings keep rate cut expectations firmly in 2027. Borrowers facing near term maturities should prioritize execution certainty as agency and life company windows remain open, but the cost of waiting continues to rise.

LA Commercial Real Estate Market TrendsWeek Ending June 19, 2026 Multifamily

- Onni Group filed plans for twin 67 story residential towers at 5700 Wilshire Blvd. in Miracle Mile, scrapping earlier office proposals in favor of 2,586 units including 197 affordable, reflecting institutional conviction in LA rental demand.

- Onni's $384M loan on the Wilshire Courtyard campus was extended to July 2026; the pending conversion play underscores how debt maturity walls are accelerating office to residential repositioning across Mid Wilshire.

- LA multifamily vacancy holds at 4.2% with 3.8% year over year rent growth; cap rates range 4.75% to 5.25% for Class A urban assets; slowing construction pipeline expected to tighten supply and support NOI growth into Q4 2026.

Retail - JH Real Estate Partners acquired the 330,000 SF FIGat7th retail center at 735 S. Figueroa St. in DTLA from Brookfield for $68.5M at $207 per SF at a 7.5% cap rate; the 86% leased center is anchored by Target, Sephora, and Zara.

- Brookfield fully retired a $61.7M MetLife loan through the sale; the deal illustrates how distressed DTLA retail with strong anchor occupancy can still trade, pricing at a significant discount to replacement cost.

- LA retail cap rates range 5.50% to 6.25% for stabilized centers; credit tenanted NNN assets with long WALT remain in demand, while Class B strip centers face prolonged vacancy as owners resist rent reductions to protect NOI.

Industrial - Walmart Realty acquired a 507,000 SF cold storage facility at 1001 Columbia Ave. in Riverside from State Street Corp. for $223M at $440 per SF; the 2010 built asset features 42 ft clear height, 98 dock doors, and 120 trailer stalls.

- The transaction allows Walmart to continue temperature controlled distribution operations; JLL noted demand for cold storage infrastructure continues to outpace supply across the Greater LA basin.

- Inland Empire overall industrial vacancy rose to 8.1% in Q1 2026; however, cold storage and last mile infill assets remain severely supply constrained, commanding premium pricing well above market averages.

Office - CBRE arranged a 55,000 SF lease at 6400 Sunset Blvd. in Hollywood; Avison Young secured a 14,361 SF office renewal with Angel City FC at Media Park Santa Monica, reflecting selective leasing in amenity rich submarkets.

- Brookfield continues to exit DTLA office as EY Plaza (725 S. Figueroa) is in receivership with over $300M in debt; Wells Fargo Center towers face maturity default with $772M combined, illustrating ongoing DTLA office distress.

- LA office vacancy exceeded 25% citywide in Q1 2026 with 400,000 SF of negative absorption; cap rates for office range 6.50% to 7.50%; adaptive reuse and office to residential conversions remain the primary value recovery strategy.

LA Market Takeaway: LA's market remains sharply bifurcated as industrial and multifamily fundamentals hold firm on tight vacancy and steady rent growth, while DTLA office continues its distress driven reset. This week's Walmart cold storage trade and Onni's residential pivot at Miracle Mile signal that institutional capital is reallocating away from legacy office into high conviction, supply constrained assets, a theme that will define LA CRE transactions through year end. |