| A Boutique Commercial Mortgage Brokerage, Dedicated to

Exceptional Service and Proven Results | |

Capital Markets Report | |

| | US Treasury Yield Curve

Month over Month Comparison |

|

|

|

|

|

|

In The News

|

|

Commercial Interest Rates and Bond Market Update

Week Ending May 1, 2026 Federal Reserve Policy

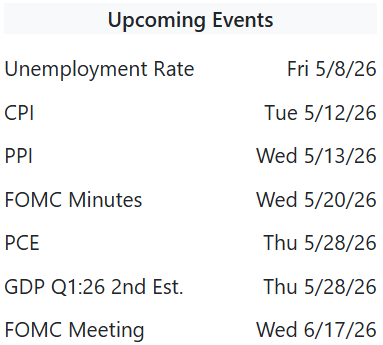

- The next FOMC meeting is scheduled for June 16 and 17, 2026, marking Kevin Warsh's first meeting as incoming Fed Chair; markets will closely watch for any policy tone shift.

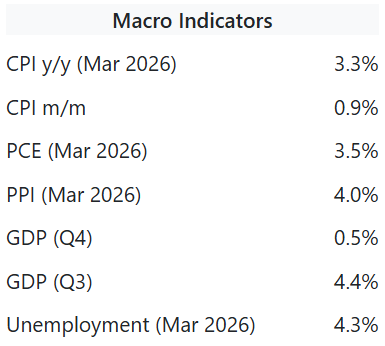

- April jobs report (May 8) and May CPI data are the next major macro indicators; March payrolls rebounded to +178K while unemployment held at 4.3%, keeping the Fed on hold.

- At its April 29 meeting, the Fed held rates at 3.50% to 3.75% amid four historic dissents; core inflation at 3.2% and Middle East conflict driven oil prices reinforced the pause.

Bond Market Trends

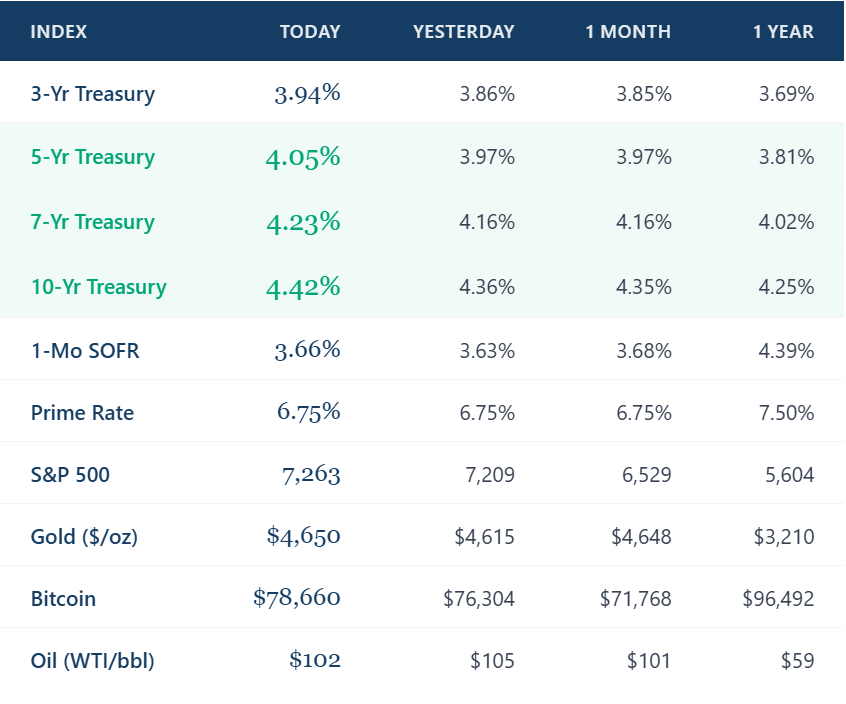

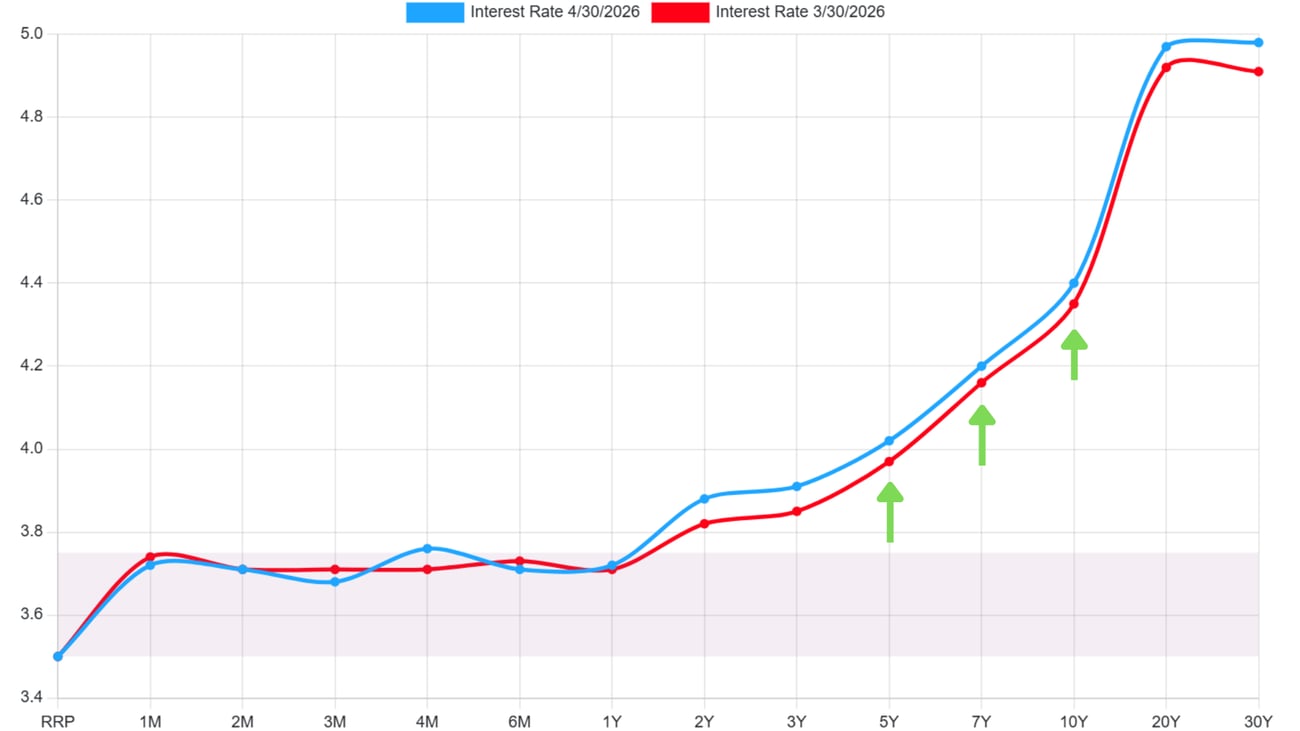

- The 5Y, 7Y, and 10Y Treasury yields each rose 4 to 5 bps month over month to 4.02%, 4.20%, and 4.40%, respectively, steepening the curve as rate cut expectations are pushed further out.

- The Fed's hawkish hold and four dissents against the easing bias drove Treasury yields higher post meeting; the 10Y hit its highest level in a month at 4.41%, reflecting tightening sentiment.

- Rising oil prices tied to the Middle East conflict and fiscal deficit concerns continue to add upward pressure on long duration Treasuries, widening the term premium across the curve.

Commercial Interest Rates

- Agency multifamily (Fannie/Freddie) rates remain in the 5.75% to 6.25% range at 65% to 70% LTV; GSE lending caps were increased 20.5% in 2026, supporting continued liquidity for stabilized deals.

- Construction loans are pricing at SOFR + 225 to 275 bps; lenders tightening proceeds on ground up projects as elevated carry costs and tepid absorption pressure stressed lease up underwriting.

- Bridge and value add debt is pricing at 7.00% to 7.75% all in; non bank lenders now represent 24% of CRE lending volume nationally, filling the gap left by tightened bank balance sheets.

Takeaway: The Fed's hawkish hold and four way dissent signal that rate cuts remain off the table until at least Q3 2026, while rising Treasury yields across the 5, 7, and 10 year benchmarks will sustain pressure on commercial borrowing costs. Sponsors should lock agency debt where available and stress test bridge assumptions against a higher for longer rate environment.

LA Commercial Real Estate Market TrendsWeek Ending May 1, 2026 Multifamily

- A 106-unit adaptive reuse property at 200 W. Ocean in Downtown Long Beach secured a $46M refinance, reflecting continued lender confidence in well located, stabilized luxury multifamily.

- Agency financing remains the dominant execution for LA multifamily; stabilized assets at 65% LTV are pricing at 5.75% to 6.00% with 1.25x DSCR, supported by 4.2% vacancy and 3.8% rent growth.

- High rates and rising construction costs are pushing LA multifamily investors from ground up development toward preservation plays and value add acquisitions of 1970s to 1980s vintage stock.

Retail

- Cedars-Sinai Medical Center acquired the Beverly Connection shopping center near its campus, signaling strong demand for infill retail with alternative use or medical conversion potential.

- Grocery anchored and necessity retail are attracting the strongest lender interest; acquisition financing is available at 55% to 60% LTV with cap rates holding in the 5.50% to 6.25% range across LA.

- Experiential and service retail continue to drive occupancy as LA consumer spending remains resilient; new supply is limited, supporting historically low vacancy and above market rent retention.

Industrial

- BLT Enterprises acquired an 81,200 SF facility in San Fernando for $31.7M ($390/SF), above the 2025 market average, highlighting premium pricing for well located SoCal infill industrial.

- Bridge Industrial secured a $60M refinance on an LA area logistics asset, reflecting continued debt fund appetite for quality industrial at 55% LTV and stabilized cash flow profiles.

- Inland Empire industrial vacancy deepened in April amid slowing absorption, though brokers note improving leasing interest; rent growth remains flat year over year as trade uncertainty weighs on tenants.

Office

- A Pasadena office building sold for $33M, as opportunistic buyers continue to target quality suburban office assets at discounted basis, well below replacement cost.

- Office refinancing remains highly selective; lenders require 70%+ occupancy, WALT of 4+ years, and sub 60% LTV; CMBS and life companies are largely inactive on CBD assets given 27%+ vacancy.

- Cushman & Wakefield reported continued occupancy losses in LA office Q1 2026; creative and media oriented product in Culver City and West LA is outperforming legacy Downtown CBD towers.

LA Market Takeaway: The LA CRE market continues to bifurcate sharply: multifamily and necessity retail benefit from tight supply, active agency lending, and resilient demand, while office and transitional industrial face headwinds from elevated vacancies and cautious debt markets. The 2028 Olympics pipeline and private capital dominance are supporting transaction momentum in well priced deals across preferred asset classes. |

|

|

| A Lesson Beyond Brokerage

| |

When the Nation Owes

More Than It Earns

|

|

| For the first time in U.S. history, the national debt has surpassed the country's entire annual economic output, meaning the federal government now owes more than every business, worker, and institution in America produces in a full year combined.

To put it in real estate terms: imagine owning a property that generates $100,000 in annual NOI, but carrying a $105,000 mortgage. The asset still functions, but your margin for error disappears and every rate increase hits harder. When debt exceeds GDP, the government faces mounting pressure to either raise taxes, cut spending, or issue more Treasury bonds to service existing obligations. More bond supply means higher yields to attract buyers. Higher yields mean higher borrowing costs across the entire economy, including commercial real estate.

This is not abstract. The elevated 10 year Treasury yield we track each week is partly a reflection of this fiscal reality. Lenders price term premium into long duration debt precisely because of this uncertainty. For our clients, the takeaway is straightforward: the era of cheap long term capital is structural, not cyclical. Underwrite accordingly, lock rates when execution is favorable, and treat current spreads as the new baseline, not a temporary condition. |

|

|  |

|

|

|

|

|

|