| A Boutique Commercial Mortgage Brokerage, Dedicated to

Exceptional Service and Proven Results | |

Capital Markets Report | |

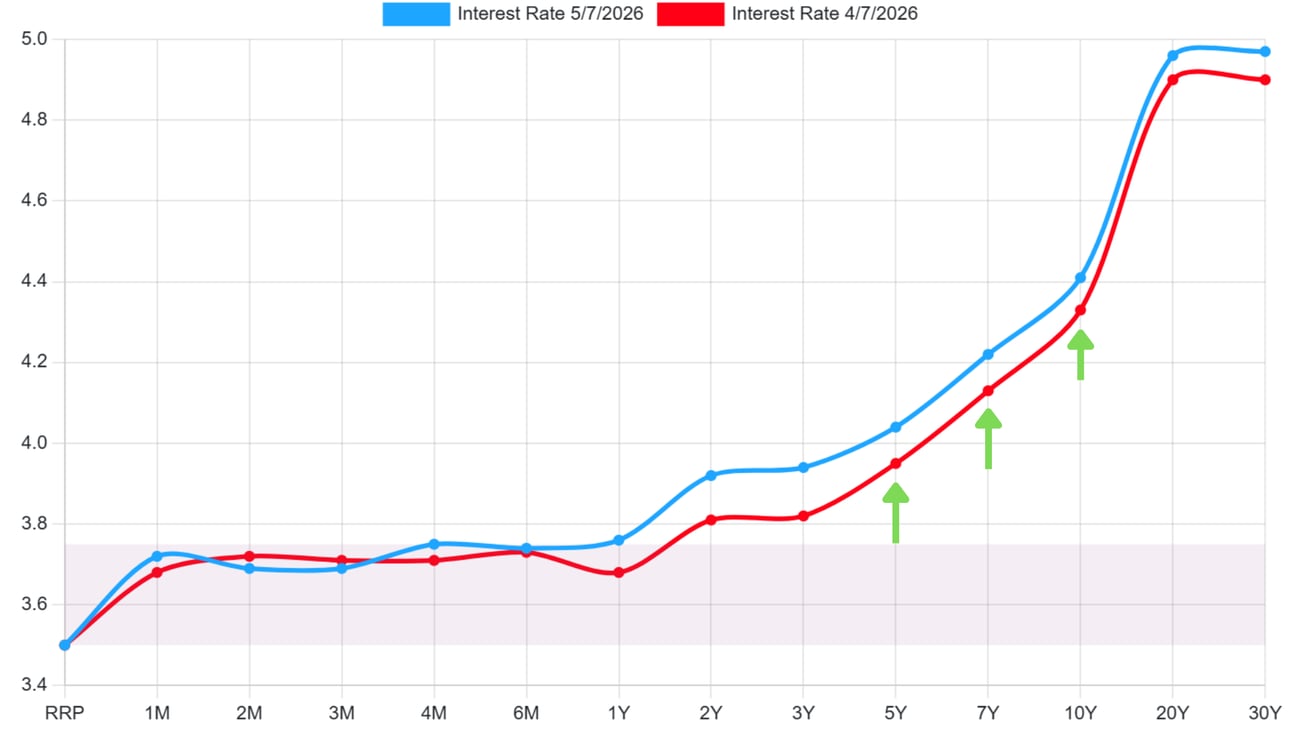

| | US Treasury Yield Curve

Month over Month Comparison |

|

|

|

|

|

|

In The News

|

|

Commercial Interest Rates and Bond Market Update

Week Ending May 8, 2026 Federal Reserve Policy

- The next FOMC meeting is June 16 and 17, Kevin Warsh's first as incoming Fed Chair; markets assign over 93% probability of another rate hold, with the Senate confirming Warsh by May 15.

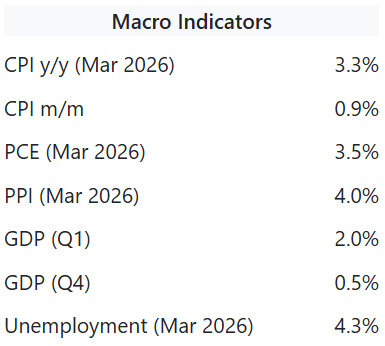

- April CPI releases mid May; April NFP came in at 115K, beating the 55K forecast, with unemployment holding at 4.3% and wage growth at 3.6% annually, signaling continued labor resilience.

- The April 29 FOMC vote, the most dissents since 1992, reflected internal division; three members opposed easing bias language, keeping the Fed funds target range at 3.50% to 3.75%.

Bond Market Trends

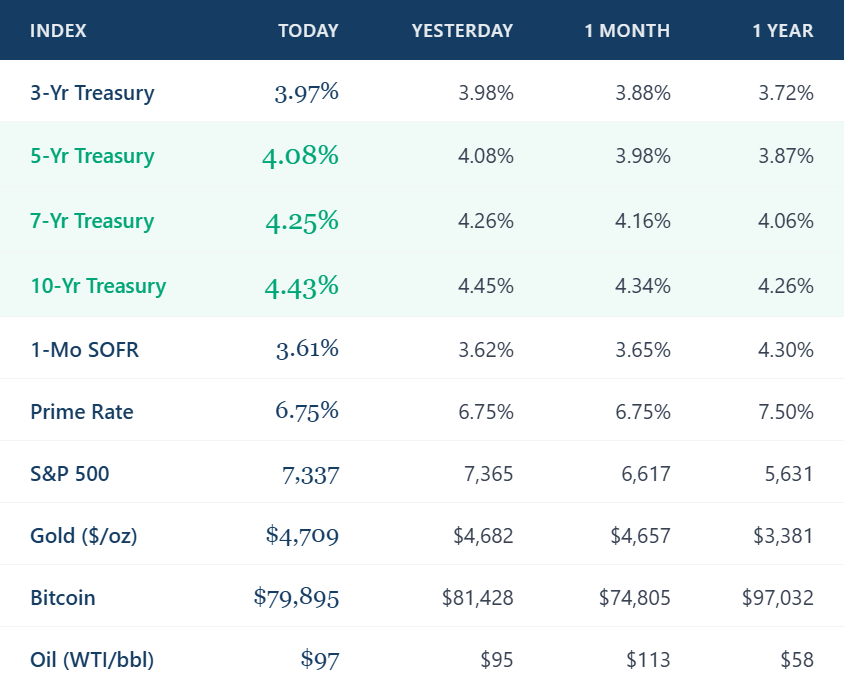

- The 5 year Treasury rose to 4.04% (from 3.95%), the 7 year climbed to 4.22% (from 4.13%), and the 10 year reached 4.41% (from 4.33%) month over month, reflecting broad long end steepening.

- Better than expected April payrolls, elevated oil prices tied to Middle East conflict, and Warsh's expected regime change at the Fed drove yields higher across intermediate and long maturities.

- The 30 year Treasury approached 4.97%; credit spreads widened modestly as institutional demand softened, and Warsh's anticipated balance sheet reduction signals further upward pressure on long rates.

Commercial Interest Rates

- Agency multifamily rates (Fannie/Freddie) are ranging 5.90% to 6.30% for 5 and 7 year fixed terms; bridge and floating rate debt remains elevated at SOFR + 275 to 350 bps amid persistent rate uncertainty.

- Construction financing is pricing at SOFR + 300 to 375 bps; lenders have tightened underwriting standards on ground up deals as rising material costs and tariff uncertainty compress development feasibility.

- Life companies remain competitive on stabilized industrial and grocery anchored retail at 60% to 65% LTV; CMBS execution has widened 15 to 20 bps this week, limiting proceeds on leveraged acquisitions.

Takeaway: The Fed's prolonged pause and leadership transition to Kevin Warsh are converging with stronger than expected labor data to keep Treasury yields elevated across the curve. For CRE borrowers, this week's yield movements, particularly in the 5 to 10 year range, are pushing all in rates higher and compressing levered returns. Borrowers with near term maturities should evaluate refinance windows carefully before Warsh's first FOMC meeting in June potentially reshapes forward rate expectations.

LA Commercial Real Estate Market TrendsWeek Ending May 8, 2026 Multifamily

- A 142 unit value add apartment complex in Koreatown traded at $27.5M ($193K/unit) at a 5.1% cap rate; the buyer plans a light renovation strategy to capture rent upside in a supply constrained submarket.

- An 88 unit 1990s built property in Van Nuys refinanced at $14.2M with a 5 year fixed rate at 6.05%, 65% LTV, and 1.25x DSCR; with rates high, investors are shifting from ground up to preservation plays.

- LA multifamily vacancy ticked down to 4.8% in Q1 2026; rent growth remains modest but stable, with GSE lending caps increased 20.5%, keeping agency debt available for qualified sponsors across submarkets.

Retail - A 22,000 SF neighborhood retail center in Burbank sold for $8.9M at a 5.6% cap rate, anchored by a regional grocer with 9 years of WALT; the asset drew multiple bids reflecting strong investor appetite for grocery anchored product.

- A mixed use strip in Culver City was acquired for $6.4M at 55% LTV with a 7 year life company loan at 6.15%; the seller carried back 10% in subordinate financing to bridge the rate environment.

- Retail vacancies remain near historic lows across LA; national soft goods and experiential tenants continue expanding in West Hollywood and Larchmont, pushing NNN asking rents above $52/SF in core corridors.

Industrial - A 78,000 SF distribution facility in Commerce sold for $19.2M ($246/SF); MSCI data shows SoCal industrial deal activity rebounding, with private capital representing 61% of all buyers across property types in the LA metro.

- A last mile logistics asset in Compton refinanced at $11.5M at 6.2% fixed, 1.30x DSCR, supported by a single tenant NNN lease through 2031; life companies remain competitive on stabilized logistics product at 60% to 65% LTV.

- LA industrial vacancy edged up modestly as new supply delivered; South Bay asking rents held near $1.42/SF/month NNN; California AB 98 regulations and trade uncertainty pose emerging headwinds to new logistics development.

Office - A creative office conversion in Culver City leased 18,000 SF to a tech firm at $5.25/SF/month gross; trophy and creative assets in premier submarkets continue to attract demand while Class B product remains challenged.

- A distressed 40,000 SF Class B office in El Segundo sold for $5.1M ($127/SF), acquired by a value add investor targeting medical or flex conversion; DTLA office valuations are down 27.3% from peak, driving adaptive reuse strategies.

- Downtown LA office vacancy remains near 26%; sublease availability continues to suppress asking rents, and debt yield requirements above 8.5% are effectively limiting new acquisition financing for most office product.

LA Market Takeaway: LA's CRE market remains bifurcated: grocery anchored retail and well located industrial continue to attract competitive capital, while office fundamentals remain deeply challenged amid high vacancy and lender caution. Multifamily fundamentals are firm, GSE lending caps are expanding and vacancy is tightening, but rising debt costs are compressing levered returns and pushing investors toward value add and preservation strategies over ground up development. |

|

|

| A Lesson Beyond Brokerage

| |

Is AI Coming for Your Job?

|

|

| The headlines are loud: AI is replacing white collar workers. And the data is starting to back it up. Information services shed 13,000 jobs in April alone, continuing a trend that has erased over 340,000 positions in that sector since late 2022, coinciding almost exactly with the rise of generative AI.

But here is what the best brokers, advisors, and dealmakers understand that the headlines miss: AI replaces tasks, not judgment. AI can pull comps, draft an OM, summarize a lease, and model a waterfall in seconds. What it cannot do is read the room in a negotiation, build trust with a hesitant seller, or structure a creative deal when the numbers do not pencil on paper. The professionals losing ground are those who built their value around information alone. The ones winning are those who use AI to move faster and think deeper, freeing their time for the relationships and decisions that actually close deals.

The threat is real. But so is the opportunity. In commercial real estate, where every transaction is personal, complex, and high stakes, human judgment is not being replaced. It is becoming more valuable than ever. | |

|  |

|

|

|

|

|

|