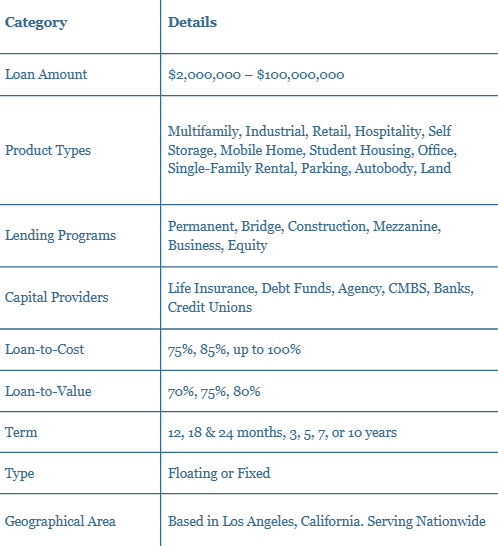

| A Boutique Commercial Mortgage Brokerage, Dedicated to

Exceptional Service and Proven Results | |

Capital Markets Report | |

| | US Treasury Yield Curve

Month over Month Comparison |

|

|

|

|

|

|

In The News

|

|

Commercial Interest Rates and Bond Market Update

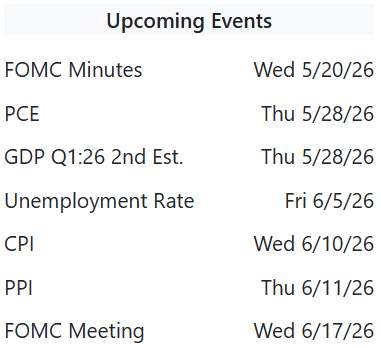

Week Ending May 15, 2026 Federal Reserve Policy

- The next FOMC meeting is June 17 and 18; markets currently price no rate cut, with Fed futures showing only a 12% probability of easing before September 2026.

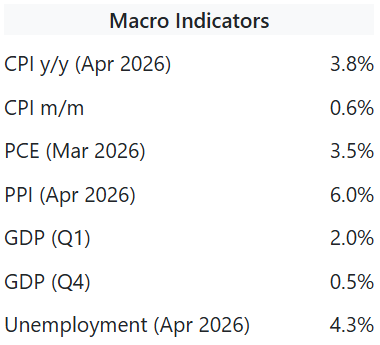

- April CPI rose 3.8% YoY, highest since May 2023, driven by a 17.9% energy surge tied to the Iran conflict; core CPI came in at 2.8%, above the 2.7% forecast.

- The April 29 FOMC statement held rates at 3.50% to 3.75%; two dissents favored cuts, but the majority cited elevated inflation as reason to stay restrictive.

Bond Market Trends

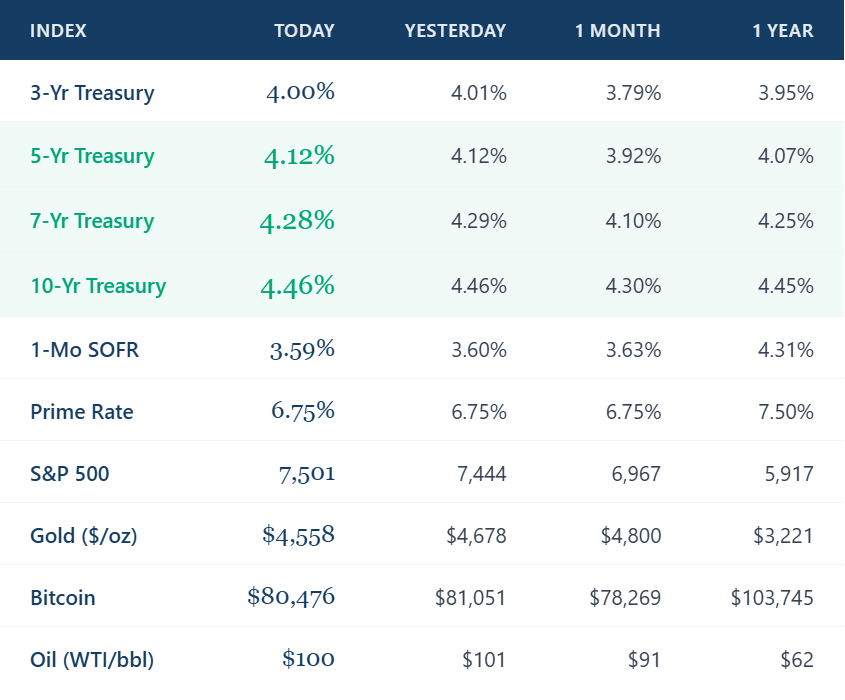

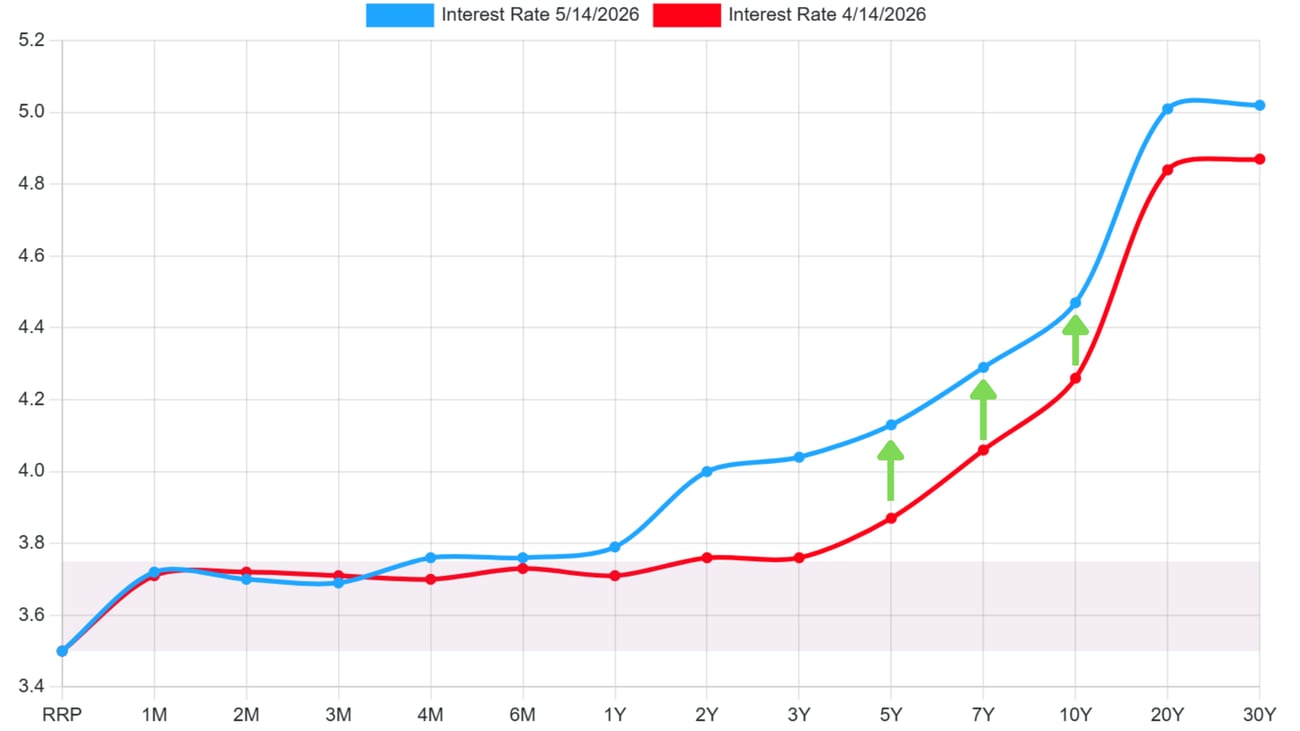

- Treasury yields rose sharply month over month: 5Y at 4.13% (from 3.87%), 7Y at 4.29% (from 4.06%), and 10Y at 4.47% (from 4.26%), reflecting persistent inflation pressure.

- The hotter than expected April CPI print released May 12 drove the 10Y yield spike; energy fueled inflation and Middle East geopolitical uncertainty are key catalysts.

- Credit spreads on investment grade bonds widened slightly to approximately 110 bps over Treasuries; CMBS spreads remain elevated, adding to all-in commercial financing costs.

Commercial Interest Rates

- Agency (Fannie/Freddie) 10-year fixed multifamily rates range 5.85% to 6.20%, with spreads of approximately 140 to 170 bps over the 10Y Treasury amid tighter GSE underwriting standards.

- Floating rate bridge and construction loans price at SOFR + 275 to 325 bps; debt funds holding LTC at 60% to 65% on new starts due to elevated refinancing risk.

- CMBS conduit executions remain active for stabilized retail and industrial; life companies competitive on industrial net lease at sub 6% fixed rates with low leverage.

Takeaway: Rising Treasury yields across the curve, driven by a surprise April CPI of 3.8% and Middle East energy shocks, are pushing all-in commercial lending rates higher heading into summer. Borrowers with upcoming maturities should engage lenders now, as rate lock opportunities may narrow if inflation remains sticky through June's CPI release.

LA Commercial Real Estate Market TrendsWeek Ending May 15, 2026 Multifamily

- A 96-unit value-add apartment complex in Koreatown traded at a 5.05% cap rate, reflecting continued investor appetite for workforce housing in supply-constrained LA submarkets.

- A stabilized 72-unit Mid-Wilshire asset closed a Fannie Mae refinance at 65% LTV, 6.00% fixed for 10 years; DSCR of 1.28x met agency underwriting requirements.

- LA multifamily vacancy holds tight at 4.2% with 3.8% YoY rent growth; Olympic infrastructure spending is catalyzing demand in East LA and Downtown corridors through 2028.

Retail

- A grocery-anchored neighborhood center in the San Fernando Valley sold for $31M at a 5.65% cap rate, supported by strong NOI from a long-term anchor lease with 9 years of WALT.

- A 14,500 SF strip center in Brentwood secured acquisition financing at 58% LTV with a 5-year fixed rate of 6.15%; lender required minimum debt yield of 8.25%.

- Retail vacancy in LA remains near historic lows; experiential and food and beverage tenants driving leasing in prime corridors like Melrose and Abbot Kinney.

Industrial

- A 110,000 SF last-mile logistics facility in Commerce sold to an institutional buyer at a 4.85% cap rate, underscoring sustained demand for infill industrial near the LA basin.

- A 185,000 SF warehouse in Vernon refinanced via CMBS at 55% LTV, 6.30% fixed; 7-year WALT lease profile and strong tenant credit supported aggressive lender pricing.

- LA industrial vacancy edged up to 4.8% as speculative deliveries absorb; rent growth moderating to 2% to 3% but South Bay and Inland Empire gateway corridors remain fundamentally tight.

Office

- A creative office campus in Culver City sold for $47M at a 6.60% cap rate; media and entertainment tenant base attracted an institutional buyer seeking stabilized creative assets.

- A West Hollywood creative office acquired bridge financing at SOFR + 295 bps, 58% LTV; borrower targeting a CMBS take-out within 18 months after lease-up of two vacant suites.

- LA overall office vacancy remains elevated at 22% plus; flight to quality persists with Class A creative space outperforming while Downtown Class B assets face prolonged lease-up headwinds.

LA Market Takeaway: LA commercial real estate activity is selectively active, with industrial and multifamily leading transaction volume amid rising financing costs. Measure ULA continues to slow high-value sales, while well-capitalized investors are finding opportunity in grocery-anchored retail and infill industrial, asset classes supported by durable demand and tight supply fundamentals heading into the 2028 Olympics cycle. |

|

|

| A Lesson Beyond Brokerage

| |

The U.S. Is Quietly Re-Industrializing (But Not Where You Think)

|

|

| The narrative around American manufacturing has shifted. Reshoring is no longer a political talking point — it is an active capital deployment strategy. But the geography of this industrial renaissance is surprising investors who are still chasing the coasts.

The real action is happening in secondary and tertiary markets. Cities like Tulsa, Columbus, El Paso, and the Carolinas are absorbing billions in advanced manufacturing investment driven by the CHIPS Act, Inflation Reduction Act incentives, and defense contractor expansion. These are not speculative bets. They are long-term, government-backed demand anchors with 15 to 25 year lease profiles.

For commercial real estate, the implications are significant. Industrial assets in these emerging corridors are being underwritten at tighter cap rates than their history would suggest, and lenders are following. Life companies and CMBS conduits are now actively quoting stabilized manufacturing facilities that would have been considered tertiary risk three years ago. The lesson for investors and brokers: do not anchor your industrial thesis to LA and the Inland Empire alone. The next decade of net absorption may be won in markets most people are not watching yet. Know the capital flows. That is where the deals will be. |

|

|  |

|

|

|

|